Vertical AI Shift

Why the next generation of AI companies will win by going deeper, not wider.

I’ve been thinking a lot about how AI value actually gets captured.

For most of the past decade, the center of gravity in AI has been horizontal. The belief was simple: whoever owns the general interface (the assistant, the inbox, the OS, the universal agent) will own the future. It felt like search all over again, or the browser wars, or the rise of mobile. The assumption was that one dominant layer would sit above everything else and aggregate all demand.

But the more I watch the market, and the more I talk to founders and operators building inside real companies, the clearer it becomes: horizontal AI has already hit its natural limits. The real leverage is shifting toward vertical AI.

This isn’t just a theoretical distinction. It’s reshaping who captures the upside of AI and who ends up being commoditized by it. Whether you’re a founder choosing a wedge, an investor evaluating defensibility, or an operator trying to stay ahead of the curve, the horizontal-vertical split shows you where the gravity is moving.

So it’s worth defining the terms clearly before going further.

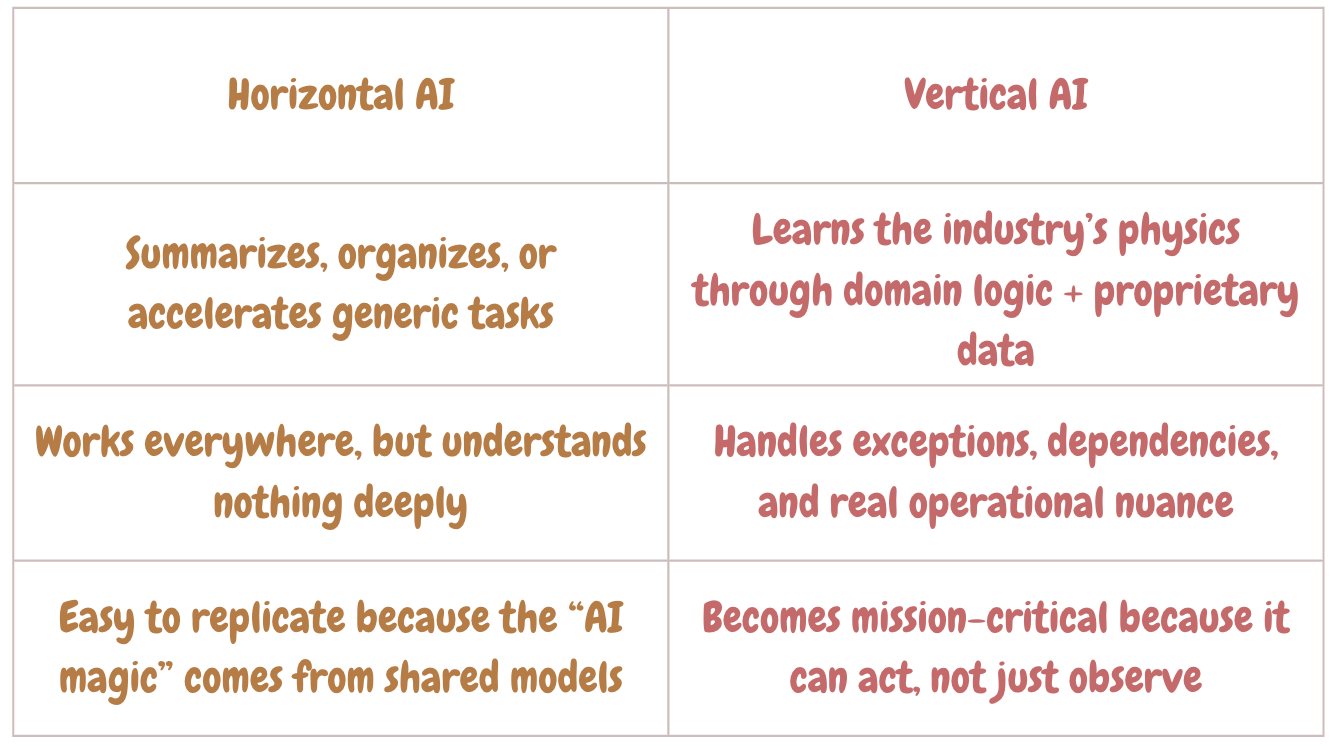

Horizontal vs. Vertical AI

People use these words casually, but there is a difference.

Horizontal AI is built to work across many industries. It handles the same general-purpose tasks everywhere: writing, summarizing, searching, coding, taking notes. It sits on top of workflows, improves them a bit, but doesn’t really understand the deeper rules beneath them. So ChatGPT, Claude, Gemini. Email copilots, document copilots, code copilots. Notion AI, Slack AI, generic meeting-note tools.

Horizontal AI is about breadth and reach. It lives as a layer on top of many different workflows, but it doesn’t own any of them.

Vertical AI is AI that is built for a specific domain, where it understands the structure, data, incentives, and edge cases of that industry. It doesn’t just answer questions about the domain; it actually runs the work.

A few examples make this clearer. In healthcare, vertical AI isn’t “summarize this visit,” but “apply the right CPT/ICD codes, validate documentation, and file a clean claim.” In logistics, it dispatches fleets, sequences routes, manages service intervals, and responds to disruptions in real time. And so on.

If I were to put this in a few words: horizontal AI sees the sentence, whereas vertical AI sees the world that produced it.

Once you see that distinction, the rest of the story starts to make more sense.

The horizontal ceiling and the vertical opportunity

The first wave of AI products looked a lot like early SaaS: quick to build, polished UI, and intentionally broad. Wrappers surfaced demand. Assistants proved people wanted intelligence in their daily tools.

But as foundation models improved, something predictable happened:

Everyone got the same baseline capabilities.

Differentiation collapsed.

Features converged.

The horizontal layer began to commoditize itself.

We’ve seen this movie before. When cloud storage first exploded, a wave of startups rushed in with “file sharing in the cloud.” For a moment, it felt like its own category. But once Google, Microsoft, and Dropbox decided to fold that feature into larger ecosystems, the standalone players evaporated almost overnight. Steve Jobs even told the Dropbox founders back in 2009 that their product was “a feature, not a company.” And within a few years, Drive, OneDrive, and iCloud made cloud storage feel less like an industry and more like a checkbox.

The same pattern repeated across other horizontal tools. Products that once felt sharp and differentiated (Evernote for notes, Slack for chat, etc) eventually got copied or absorbed into larger suites. Slack built something genuinely novel, but the moment Microsoft bundled Teams for free with Office 365, the gravitational pull of another platform took over. Slack didn’t disappear, but the platform dynamics shifted enough that selling became the most rational outcome.

Horizontal categories always face this gravity. If your edge comes from a general-purpose model that every competitor can license, the moat collapses as soon as the underlying infrastructure converges.

Horizontal AI is easy to start (APIs do most of the work) but painfully hard to defend.

Because in real operations, context determines everything. A horizontal model can give you information; a vertical model can run the workflow. A general AI might detect that a truck is delayed, but a vertical logistics AI knows exactly why it matters and what action to take. A horizontal AI can summarize a doctor’s visit; a vertical healthcare AI extracts the implied diagnosis code, checks payer rules, updates the record, and initiates billing.

This is the real split.

That’s where the opportunity is moving. Horizontal AI is heading toward “good enough everywhere,” which is just a polite way of saying “commodity.” Meanwhile, every industry is full of high-friction workflows begging for an AI system that doesn’t just describe the work, but actually does it.

The best vertical SaaS companies have always embedded themselves into the workflow and accumulated data that rivals couldn’t copy. AI accelerates that motion: systems-of-record (“what happened?”) are evolving into systems-of-action (“what should I do right now?”). We’re already seeing products shift from dashboards to operators; software that resolves issues automatically and surfaces next-best actions in real time.

That’s the frontier. Not AI that sits above everything, but AI that digs into one domain deeply enough to become its backbone.

Workflows as the new center of gravity

In the AI era, I think the real moat won’t come from having the most advanced model, but it will come from owning the workflow.

A workflow is the end-to-end way an industry actually functions: how money moves, how risk is managed, how decisions get made, and all the unspoken norms and ugly edge cases that only insiders ever see. When your software becomes that, you’re no longer a tool; you’re the backbone. Removing you isn’t a product switch, but a full operational upheaval.

Look at Procore in construction. It didn’t win by offering “project management with AI.” It won by gradually becoming the operating system of the job site: drawings, RFIs, submittals, inspections, schedules, budgets, safety logs, compliance, the whole stack. Once Procore is embedded, ripping it out is like trying to rebuild a skyscraper mid-construction. You don’t replace it; you plan your project around it.

Veeva did the same thing in life sciences. Salesforce had a massive head start in CRM. But Veeva didn’t just build a prettier Salesforce; it built a CRM that understood pharma with sample management, KOL education programs, clinical trial documentation, FDA/EMA compliance, controlled content workflows. Coming “out-of-the-box” with industry-specific validation rules made it instantly usable in a sector where mistakes can trigger regulatory action. No horizontal CRM could match that. It’s why nearly every major pharmaceutical company adopted Veeva, and why Salesforce’s late entry with “Life Sciences Cloud” still can’t match the fidelity of something that lives inside the workflow instead of on the surface.

This is the lesson: when you own the workflow, you own the customer.

Because replacing you isn’t switching vendors, it’s rewiring how the business actually operates.

So it is software evolving from observer to operator.

It works because the best vertical AI companies don’t just model language, they model the logic of an industry: the constraints, incentives, exceptions, dependencies, and the weird edge cases humans only learn after years in the trenches. Once your AI is making decisions and performing work inside that system, removing it becomes almost unthinkable. At that point, it’s not software anymore; it’s a part of your workforce.

And that’s where the next generation of defensibility will come from.

The layer the market is undervaluing

Over the past couple of years, most of the hype (and most of the money) has gone to the parts of AI farthest from where real economic value sits. Investors rushed into giant model labs burning through absurd amounts of capital, betting that scale alone would create a moat. Others got swept up in the excitement around “general-purpose agents” that look magical in demos but fall apart the minute they meet a real workflow.

And then came the flood of horizontal wrapper apps → quick-to-ship copilots that add a thin UI on top of the same LLM APIs. They attracted a ton of FOMO capital, but they’re also the easiest to copy. When everyone uses the same models and targets the same broad audience, everything starts to blur together.

Meanwhile, the part of the stack closest to real work (vertical, domain-specific applications) has been strangely overlooked. That’s the irony: it’s the layer with the clearest path to durable defensibility.

Vertical software used to be dismissed as “niche,” but companies like Veeva, Procore, Toast, etc proved that going deep into one industry creates bigger markets, stronger loyalty, and far fewer competitors.

AI is now following the same pattern.

Infra got overhyped first. Horizontal copilots had their moment.

And now the shift is happening quietly: toward AI built around specific workflows and actual business problems.

Investors who are paying attention already see the pattern:

Vertical AI builds real moats from proprietary industry data and domain expertise.

Horizontal AI relies on UI differences or distribution → neither of which last.

Specialized datasets (claims, contracts, supply-chain logs, clinical notes) are becoming the real separator.

I’d honestly argue that if there’s an AI bubble anywhere, then it’s in the generic layers closest to the hype.

The undervalued layer is the one embedded inside the workflow, shaping decisions and driving revenue.

We’ve seen this play out before. Cloud software went through the same arc: infrastructure first, horizontal SaaS next, then the quiet rise of massive vertical winners once the hype cooled. AI is entering that same phase now.

The vertical phase

Every major technology wave eventually moves from broad general-purpose tools to deep, industry-shaped systems. It happened with the internet, with mobile, with the cloud. And AI is hitting that phase faster simply because the infrastructure matured overnight.

Horizontal AI will remain important. It becomes the substrate. But value drifts toward the workflows, where AI can actually make decisions, bend cost curves, reduce friction, and change how an industry behaves.

The companies that understand this won’t be building chatbots. They’ll be rebuilding how logistics networks operate, how clinics run, how underwriting is done, how maintenance is scheduled, how compliance gets handled.

They won’t look like “AI companies” at first. They’ll look like operators who understand their industries better than anyone else, and happen to have an AI engine running under the hood.

And that’s the quiet shift happening now: the next generation of AI companies won’t try to sit above the workflow. They’ll become the workflow. And once they do, they won’t just participate in the industry - they’ll define it.

Thanks for the great writeup, Nouf!

I actually have a different view on this topic, as I think it’s becoming increasingly difficult for startups to build strong vertically integrated products.

To frame the discussion, here are my thoughts:

I don’t see agents as the new apps. Apps aren’t going away, while the agent layer itself will likely be dominated by large companies, as it feels like a natural progression of foundation model capabilities rather than a layer startups can sustainably own. Over time, horizontal agents will outperform vertical, domain-specific ones as foundation models become better at understanding context across domains. Because of that, owning the agent layer within a vertical won’t be a long-term advantage.

The real defensible moats for AI-first vertical products are either deep integration with physical operations or operating in heavily regulated spaces (e.g. fintech).

As for AI-first products more broadly, I believe the more sustainable path is FDE-style distribution rather than trying to build standalone agent-driven products.